Filed Pursuant to

Rule 424(b)(3)

Registration

Statement no. 333-256450

PROSPECTUS

22,643,678 Subordinate Voting Shares

Lowell Farms Inc.

This prospectus relates to 22,643,678 Subordinate Voting Shares of

Lowell Farms Inc., a British Columbia, Canada corporation, that may

be sold from time to time by the selling securityholders set forth

in this prospectus under the heading “Selling

Securityholders” beginning on page 23 which we refer to as the “Selling

Securityholders.”

We will not receive any proceeds from the sale of the securities

under this prospectus.

Information regarding the Selling Securityholders, the amounts of

Subordinate Voting Shares that may be sold by them and the times

and manner in which they may offer and sell the Subordinate Voting

Shares under this prospectus is provided under the sections titled

“Selling Securityholders” and “Plan of

Distribution,” respectively, in this prospectus. We have not

been informed by any of the Selling Securityholders that they

intend to sell their securities covered by this prospectus and do

not know when or in what amounts the Selling Securityholders may

offer the securities for sale. The Selling Securityholders may sell

any, all, or none of the securities offered by this

prospectus.

The Selling Securityholders and intermediaries through whom such

securities are sold may be deemed “underwriters” within

the meaning of the Securities Act of 1933, as amended, with respect

to the securities offered hereby, and any profits realized or

commissions received may be deemed underwriting compensation. We

have agreed to indemnify the Selling Securityholders against

certain liabilities, including liabilities under the Securities

Act.

The Subordinate Voting Shares are listed for trading on the

Canadian Securities Exchange (“CSE”) under the symbol

“LOWL” and are traded over-the-counter in the United

States on the OTCQX under the symbol “LOWLF.” On May

17, 2021, the last reported sale price of our Subordinate Voting

Shares on the CSE was C$1.45 per share.

Investing in our securities involves a high degree of risk. See the

section titled “Risk Factors,” which begins on

page 8.

Neither the Securities and Exchange Commission nor any state

securities commission has approved or disapproved of these

securities or determined if this prospectus is truthful or

complete. Any representation to the contrary is a criminal

offense.

You should rely only on the information contained in this

prospectus. We have not authorized any dealer, salesperson or other

person to provide you with information concerning us, except for

the information contained in this prospectus. The information

contained in this prospectus is complete and accurate only as of

the date on the front cover page of this prospectus, regardless of

the time of delivery of this prospectus or the sale of any

securities. This prospectus is not an offer to sell these

securities and we are not soliciting an offer to buy these

securities in any state where the offer or sale is not

permitted.

The date of this prospectus is June 3, 2021

TABLE OF CONTENTS

|

FORWARD-LOOKING STATEMENTS

|

5

|

|

ABOUT

THIS PROSPECTUS

|

5

|

|

PROSPECTUS SUMMARY

|

5

|

|

THE OFFERING

|

7

|

|

RISK FACTORS

|

8

|

|

USE OF PROCEEDS

|

22

|

|

SELLING SECURITYHOLDERS

|

23

|

|

DESCRIPTION OF BUSINESS

|

24

|

|

DESCRIPTION OF PROPERTY

|

40

|

|

CORPORATE INFORMATION

|

40

|

|

LEGAL PROCEEDINGS

|

43

|

|

MARKET PRICE AND DIVIDENDS ON COMMON EQUITY AND RELATED STOCKHOLDER

MATTERS

|

43

|

|

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION

AND RESULTS OF OPERATIONS

|

44

|

|

DIRECTORS AND EXECUTIVE OFFICERS

|

64

|

|

EXECUTIVE COMPENSATION

|

66

|

|

CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS

|

69

|

|

SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND

MANAGEMENT

|

70

|

|

PLAN OF DISTRIBUTION

|

72

|

|

CERTAIN UNITED STATES FEDERAL INCOME TAX CONSIDERATIONS

|

73

|

|

CANADIAN TAX CONSIDERATIONS

|

78

|

|

DESCRIPTION OF SECURITIES TO BE REGISTERED

|

80

|

|

INTERESTS OF NAMED EXPERTS AND COUNSEL

|

82

|

|

LEGAL MATTERS

|

82

|

|

EXPERTS

|

82

|

|

HOW TO GET MORE INFORMATION

|

82

|

|

INDEX TO FINANCIAL STATEMENTS

|

F-1

|

|

INDEX TO PRO FORMA FINANCIAL STATEMENT

|

PF-1

|

FORWARD-LOOKING STATEMENTS

This registration statement includes “forward-looking

information” and “forward-looking statements”

within the meaning of Canadian securities laws and United States

securities laws (collectively, “forward-looking

statements”). In some cases, you can identify these

statements by forward-looking words such as “may”,

“will”, “would”, “could”,

“should”, “believes”,

“estimates”, “projects”,

“potential”, “expects”,

“plans”, “intends”,

“anticipates”, “targeted”,

“continues”, “forecasts”,

“designed”, “goal”, or the negative of

those words or other similar or comparable words. Any statements

contained in this registration statement that are not statements of

historical facts may be deemed to be forward-looking statements. We

have based these forward-looking statements largely on our current

expectations and projections about future events and financial

trends that we believe may affect our business, financial

condition, results of operations and future growth

prospects. The forward-looking statements contained

herein are based on certain key expectations and assumptions,

including, but not limited to, with respect to expectations and

assumptions concerning receipt and/or maintenance of required

licenses and third party consents and the success of our

operations, are based on estimates prepared by us using data from

publicly available governmental sources, as well as from market

research and industry analysis, and on assumptions based on data

and knowledge of this industry that we believe to be reasonable.

These forward-looking statements are not guarantees of future

performance or development and involve known and unknown risks,

uncertainties and other factors that are in some cases beyond our

control. As a result, any or all of our forward-looking statements

in this registration statement may turn out to be inaccurate.

Factors that may cause actual results to differ materially from

current expectations include, among other things, those listed

under “Risk Factors.” Except as required by law, we

assume no obligation to update or revise these forward-looking

statements for any reason, even if new information becomes

available after the date of this registration statement. You

should, however, review the factors and risks we describe in the

reports we will file from time to time with the SEC after the date

of this registration statement.

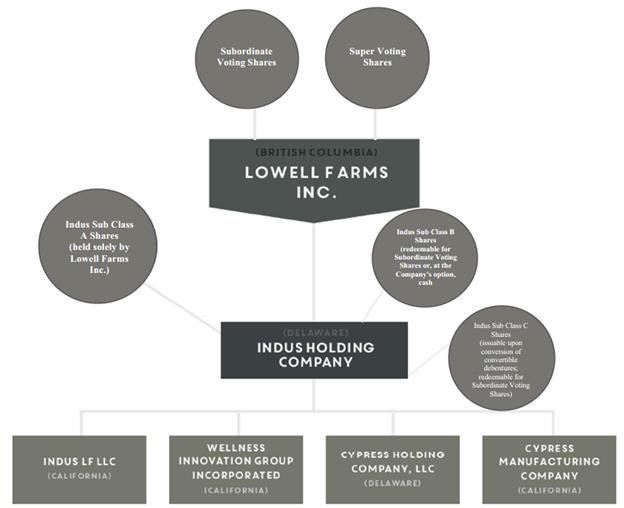

ABOUT THIS PROSPECTUS

Unless the context indicates or suggests otherwise, references to

“we,” “our,” “us,” the

“Company,” or “Lowell Farms” refer to

Lowell Farms Inc., a corporation organized under the laws of

British Columbia, Canada, individually, or as the context requires,

collectively with its subsidiaries. We changed our name from Indus

Holdings, Inc. to Lowell Farms Inc, effective March 1, 2021. For a

discussion of our corporate history, see “Corporate

Information” beginning on page 40 below.

In this prospectus, currency amounts are stated in U.S. dollars

(“$”), unless specified otherwise. All references to C$

are to Canadian dollars.

PROSPECTUS SUMMARY

This summary does not contain all of the information that is

important to you. You should read the entire prospectus, including

the Risk Factors and our consolidated financial statements and

related notes appearing elsewhere in this prospectus before making

an investment decision.

General

We are a California-based cannabis company with vertically

integrated operations including large scale cultivation,

extraction, processing, manufacturing, branding, packaging and

wholesale distribution to retail dispensaries. We manufacture and

distribute proprietary and third-party brands throughout the State

of California, the largest cannabis market in the world. We also

provide manufacturing, extraction and distribution services to

third-party cannabis and cannabis branding companies. We operate a

225,000 square foot greenhouse cultivation facility in Monterey

County, a 15,000 square foot manufacturing and laboratory facility

in Salinas, California, a separate 20,000 square foot distribution

facility in Salinas, California and a warehouse depot and

distribution vehicles in Los Angeles, California.

On February 25, 2021, we acquired the Lowell Herb Co. and Lowell

Smokes trademark brands, product portfolio and production assets

from The Hacienda Company, LLC, a California limited liability

company (“Hacienda”), and its subsidiaries. The

acquisition is referred to in this Form S-1 as the “Lowell

Acquisition.” The Lowell Acquisition expanded our product

offerings by adding a highly regarded, mature line of premium

branded cannabis pre-rolls, including infused pre-rolls, to our

product portfolio under the Lowell Herb Co. and Lowell Smokes

brands. The Lowell Acquisition also expanded our offerings of

premium packaged flower, concentrates, and vape products. We

believe our pre-existing strengths in cultivation and sourcing will

enhance the value of the brands and products acquired in the Lowell

Acquisition.

The Lowell Acquisition also substantially broadened our customer

base by adding highly developed direct-to-consumer channels to

complement our pre-existing network of retail dispensary customers.

This addition to our customer base has resulted in broader

geographic coverage in California by the combined

business.

Corporate Information

We are incorporated under the laws of British Columbia, Canada. On

April 26, 2019, we completed a reverse takeover transaction with

Indus Holding Company, a Delaware corporation. On March 1, 2021, in

connection with the Lowell Acquisition, we changed our name to

Lowell Farms Inc.

THE OFFERING

|

Subordinate

Voting Shares Offered:

|

|

22,643,678

|

|

|

|

|

|

Outstanding

Subordinate Voting Shares:

|

|

70,612,253

|

|

|

|

|

|

Use of

Proceeds:

|

|

We are not

selling any securities under this prospectus and we will not

receive any proceeds from any sale of securities by the Selling

Securityholders.

|

|

|

|

|

|

CSE Symbol for

Subordinate Voting Shares:

|

|

LOWL

|

|

|

|

|

|

OTCQX Symbol

for Subordinate Voting Shares:

|

|

LOWLF

|

RISK FACTORS

Investing in our securities involves a high degree of risk.

Investors should carefully consider the risks described below and

all of the other information set forth in this Registration

Statement on Form S-1, including our financial statements and

related notes and “Management’s Discussion and Analysis

of Financial Condition and Results of Operations,” before

deciding to invest in our common stock. If any of the events or

developments described below occur, our business, financial

condition, or results of operations could be materially or

adversely affected. As a result, the market price of our common

stock could decline, and investors could lose all or part of their

investment.

Risks Related to Our Business and Industry

Cannabis Continues to be a Controlled Substance under the CSA and

is Illegal Under United States federal law.

The Company is engaged directly in the medical and adult-use

cannabis industry. The Company derives all of its revenues from the

State of California and conducts its activities in accordance with

applicable state and local laws. Even though the Company’s

cannabis-related activities are compliant with applicable state and

local law, such activities remain illegal under U.S. federal

law.

In the United States, cannabis is extensively regulated at the

state level. 36 States, the District of Columbia and four US

territories have legalized medical cannabis in some form. Of these

States, 15 States, including California, have legalized cannabis

for adult use. Notwithstanding the permissive regulatory

environment of cannabis at the State level, cannabis continues to

be categorized as a Schedule I controlled substance under the CSA

and as such, the cultivation, manufacture, distribution, sale and

possession of cannabis violates federal law. Although the Company

believes its business is compliant with applicable State and local

law, strict compliance with state and local laws with respect to

cannabis may not absolve the Company of liability under federal

law, nor may it provide a defense to any federal proceeding which

be brought against the Company. Any such proceedings brought

against the Company may result in a material adverse effect on the

Company.

Since the cultivation, manufacture, distribution, sale and

possession of cannabis is illegal under federal law, the Company

may be deemed to be aiding and abetting illegal activities. Under

these circumstances, U.S. law enforcement authorities, in their

attempt to regulate the illegal use of cannabis, may seek to bring

an action or actions against the Company, including, but not

limited to, a claim regarding the possession and sale of cannabis,

and/or aiding and abetting another’s criminal activities. The

federal law provides that anyone who “commits an offense or

aids, abets, counsels, commands, induces or procures its

commission, is punishable as a principal.” As a result, the

DOJ could allege that Lowell Farms has “aided and

abetted” violations of federal law by providing financing and

services to its subsidiaries. Under these circumstances, a federal

prosecutor could seek to seize the assets of the Company, and to

recover any “illicit profits” previously distributed as

of such time to shareholders resulting from any of the foregoing.

In these circumstances, the Company’s operations would cease,

shareholders could lose their entire investment and directors,

officers and/or shareholders may be left to defend any criminal

charges against them at their own expense and, if convicted, be

sent to federal prison. Such potential criminal liability of our

shareholders could arise solely by virtue of their activities as

shareholders. Such an action would result in a material adverse

effect on the Company.

The United States Customs and Border Protection (“CBP”)

enforces the laws of the United States. Crossing the border while

in violation of the CSA and other related federal laws may result

in denied admission, seizures, fines and apprehension. CBP officers

administer the Immigration and Nationality Act to determine the

admissibility of travelers, who are non-U.S. citizens, into the

United States. An investment in the Company, if it became known to

CBP, could have an impact on a shareholder’s admissibility

into the United States and could lead to a lifetime ban on

admission.

Enforcement of U.S. Federal Law Could Damage the Company’s

Operations and Financial Position.

Since 2014, the United States Congress has passed appropriations

bills that have included the Rohrabacher-Farr Amendment. For now,

the Rohrabacher-Farr Amendment, as discussed above, is the only

statutory restraint on enforcement of federal cannabis laws. Courts

in the U.S. have construed these appropriations bills to prevent

the federal government from prosecuting individuals or businesses

when those individuals or businesses operate in strict compliance

with state and local medical cannabis regulations; however, this

legislation only covers medical cannabis, not adult-use cannabis,

and has historically been passed as an amendment to omnibus

appropriations bills, which by their nature expire at the end of a

fiscal year or other defined term.

The Rohrabacher-Farr Amendment may or may not be included in future

omnibus appropriations packages or continuing budget resolutions,

and its inclusion or non-inclusion, as applicable, is subject to

political changes. Because this conduct continues to violate

federal law, U.S. courts have observed that should the Congress at

any time choose to appropriate funds to fully prosecute the CSA,

any individual or business - even those that have fully complied

with State law - could be prosecuted for violations of federal law

and if the Congress restores such funding, the federal government

will have the authority to prosecute individuals and businesses for

violations of the law while it lacked funding, to the extent of the

CSA’s five-year statute of limitations applicable to

non-capital CSA violations. The Company may be irreparably harmed

by any change in enforcement policies by the federal or applicable

state governments, which could have a material adverse effect on

the Company’s business, revenues, operating results and

financial condition as well as the Company’s

reputation.

Violations of any federal laws and regulations could result in

significant fines, penalties, administrative sanctions, convictions

or settlements arising from civil proceedings conducted by either

the federal government or private citizens, or criminal charges,

including, but not limited to, disgorgement of profits, cessation

of business activities or divestiture. This could have a material

adverse effect on the Company, including its reputation and ability

to conduct business, its holding (directly or indirectly) of

cannabis licenses in California, the listing of its securities on

any stock exchange, its financial position, operating results,

profitability or liquidity or the market price of its shares. In

addition, it will be difficult for the Company to estimate the time

or resources that would be needed in connection with the

investigation of any such matters or its final resolution because,

in part, the time and resources that may be needed are dependent on

the nature and extent of any information requested by the

applicable authorities involved, and such time or resources could

be substantial.

As a result of the conflicting views between states and the federal

government regarding cannabis, investments in cannabis businesses

in the U.S. are subject to inconsistent legislation and regulation.

The response to this inconsistency was addressed in Cole

Memorandum, acknowledging that notwithstanding the designation of

cannabis as a controlled substance at the federal level in the

United States, several U.S. states had enacted laws relating to

cannabis for medical purposes. The Cole Memorandum outlined certain

enforcement priorities for the DOJ relating to the prosecution of

cannabis offenses. In particular, the Cole Memorandum noted that in

jurisdictions that have enacted laws legalizing cannabis in some

form and that have also implemented strong and effective regulatory

and enforcement systems to control the cultivation, manufacturing,

distribution, sale and possession of cannabis, conduct in

compliance with those laws and regulations is less likely to be a

priority at the federal level. Notably, however, the DOJ did not

provide specific guidelines for what regulatory and enforcement

systems it deemed sufficient under the Cole Memorandum

standard.

In light of limited investigative and prosecutorial resources, the

Cole Memorandum concluded that the DOJ should be focused on

addressing only the most significant threats. States where cannabis

had been legalized were not characterized as a high priority. In

March 2017, the then newly appointed Attorney General Jeff Sessions

again noted limited federal resources and acknowledged that much of

the Cole Memorandum had merit; however, he disagreed that it had

been implemented effectively. Accordingly, on January 4, 2018,

Attorney General Sessions issued the Sessions Memorandum, which

rescinded the Cole Memorandum on the basis that the direction

provided therein was unnecessary, given the well-established

principles governing federal prosecution that are already in place.

Those principals are included in chapter 9-27-000 of the United

States Attorneys’ Manual and require federal prosecutors

deciding which cases to prosecute to weigh all relevant

considerations, including federal law enforcement priorities set by

the Attorney General, the seriousness of the crime, the deterrent

effect of criminal prosecution and the cumulative impact of

particular crimes on the community. Due to the ambiguity of the

Sessions Memorandum and the lack of clarity provided by the DOJ

since then, there can be no assurance that the federal government

will not seek to prosecute cases involving cannabis businesses that

are otherwise compliant with State law.

The effect of the rescission of the Cole Memorandum remains to be

seen. Currently, federal prosecutors are free to utilize their

prosecutorial discretion to decide whether to prosecute cannabis

activities despite the existence of state-level laws that may be

inconsistent with federal prohibitions. No direction was given to

federal prosecutors in the Sessions Memorandum as to the priority

they should ascribe to such cannabis activities, and resultantly it

is uncertain how active federal prosecutors will be in relation to

such activities. While some U.S. Attorneys expressed support for

the rescission of the Cole Memorandum, numerous government

officials, legislators and federal prosecutors in states with

medical and adult-use cannabis statutes announced their intention

to continue the Cole Memorandum-era status quo.

The impact that this lack of uniformity between state and federal

authorities could have on individual state cannabis markets and the

businesses that operate within them is unclear, and the enforcement

of relevant federal laws is a significant risk. Potential federal

prosecutions could involve significant restrictions being imposed

upon the Company or third parties, while diverting the attention of

key executives. Such proceedings could have a material adverse

effect on the Company’s business, revenues, operating results

and financial condition, as well as the Company’s reputation

and prospects, even if such proceedings were concluded successfully

in favor of the Company. Such proceedings could involve the

prosecution of key executives of the Company or the seizure of

corporate assets.

With a new administration at the U.S. federal level, it is possible

that additional changes (whether positive or negative) could occur.

There can be no assurance as to the position any new administration

may take on marijuana and a new administration could decide to take

a stronger approach to the enforcement of federal laws. Any

enforcement of current federal laws could cause significant damage

to the Company’s operations and financial position. Further,

future presidential administrations may want to treat marijuana

differently and potentially enforce the federal laws more

aggressively.

The Rohrabacher-Farr Amendment may not be Renewed Potentially

Resulting in DOJ Enforcement Activities Against Entities in the

Cannabis Industry.

The Rohrabacher-Farr Amendment, as discussed above, prohibits the

DOJ from spending funds appropriated by Congress to enforce the

tenets of the CSA against the medical cannabis industry in states

which have legalized such activity. On December 27, 2020, the

amendment was renewed through the signing of the fiscal year 2021

omnibus spending bill and is effective through September 30, 2021.

There can be no assurance that the federal government will not seek

to prosecute cases involving medical cannabis businesses that are

otherwise compliant with state law. Such potential proceedings

could involve significant restrictions being imposed upon the

Company or third parties, while diverting the attention of key

executives. Such proceedings could have a material adverse effect

on the Company, even if such proceedings were concluded

successfully in favor of the Company.

Federal and State Forfeiture Laws Could Result in Seizure of our

Assets.

As an entity that conducts business in the cannabis industry, the

Company is subject to U. S. federal and state forfeiture laws

(criminal and civil) that permit the government to seize the

proceeds of criminal activity. Civil forfeiture laws could provide

an alternative for the federal government or any state (or local

police force) that wants to discourage residents from conducting

transactions with cannabis related businesses but believes criminal

liability is too difficult to prosecute. Also, an individual can be

required to forfeit property considered to be the proceeds of a

crime even if the individual is not convicted of the crime, and the

standard of proof in a civil forfeiture matter is lower than the

standard in a criminal matter. Shareholders of the Company located

in jurisdictions where cannabis remains illegal may be at risk of

prosecution under federal and/or state conspiracy, aiding and

abetting, and money laundering statutes, and be at further risk of

losing their investments or proceeds under forfeiture statutes.

Many states remain fully able to take action to prevent the

proceeds of cannabis businesses from entering their state. Because

state legalization is relatively new, it remains to be seen whether

these states would take such action and whether a court would

approve it. Current and prospective securityholders of the Company

or any entity related thereto should be aware of these potentially

relevant federal and State laws in considering whether to remain

invested or invest in the Company or any entity related

thereto.

Future Research may Lead to Findings that Vaporizers, Electronic

Cigarettes and Related Products are not Safe for Their Intended

Use.

Vaporizers, electronic cigarettes and related products were

recently developed and therefore the scientific or medical

communities have had a limited period of time to study the

long-term health effects of their use. Currently, there is limited

scientific or medical data on the safety of such products for their

intended use and the medical community is still studying the health

effects of the use of such products, including the long-term health

effects. If the scientific or medical community were to determine

conclusively that use of any or all of these products pose

long-term health risks, market demand for these products and their

use could materially decline. Such a determination could also lead

to litigation, reputational harm and significant regulation. Loss

of demand for our product, product liability claims and increased

regulation stemming from unfavorable scientific studies on cannabis

vaporizer products could have a material adverse effect on our

business, results of operations and financial

condition.

We May Have Limited Access to Capital as a Result of our Business

and Operations.

Because the Company cultivates, processes, possesses, and

distributes cannabis products in violation of the CSA, a

significant proportion of providers of debt and equity capital are

unwilling or unable to enter into financing transactions with the

Company. As a result, the Company’s access to capital is and

may continue to be extremely limited, which inhibits the ability of

the Company to fund operations and investments in growth

initiatives. The Company’s financial results, financial

condition, business and prospects are and may continue to be

materially adversely affected by its inability to access

capital.

Anti-Money Laundering Laws and Regulations May Limit Access to

Traditional Banking Funds and Services.

The Company is subject to a variety of laws and regulations in the

U.S. and Canada that involve money laundering, financial

recordkeeping and proceeds of crime, including the Bank Secrecy

Act, as amended by Title III of the Uniting and Strengthening

America by Providing Appropriate Tools Required to Intercept and

Obstruct Terrorism Act of 2001 (USA PATRIOT Act), the U.S.

Anti-Money Laundering Laws, 18 U.S.C. §§ 1956, 1957, the

Proceeds of Crime (Money Laundering) and Terrorist Financing Act

(Canada), as amended and the rules and regulations promulgated

thereunder, the Criminal Code (Canada) and any related or similar

rules, regulations or guidelines, issued, administered or enforced

by governmental authorities in the U.S. and Canada. Further, under

federal law, banks or other financial institutions often refuse to

provide a checking account, debit or credit card, small business

loan, or any banking services that could be found guilty of

money-laundering, aiding and abetting or conspiracy to businesses

involved in the cannabis industry due to the present state of the

laws and regulations governing financial institutions in the U.S.

The lack of banking and financial services presents unique and

significant challenges to businesses in the U.S. cannabis industry.

While Lowell Farms has maintained bank accounts, the loss of such

accounts and the potential lack of a secure place in which to

deposit and store cash, the inability to pay creditors through the

issuance of checks and the inability to secure traditional forms of

operational financing, such as lines of credit, are some of the

many challenges presented to U.S. cannabis companies, and which

could conceivably impact the Company, by the unavailability of

traditional banking and financial services.

Despite these laws, FinCEN issued the FinCEN Guidance in 2014,

which as described above, outlines the pathways for financial

institutions to bank state sanctioned cannabis businesses in

compliance with federal enforcement priorities. The FinCEN Guidance

echoed the enforcement priorities of the Cole Memorandum. Under

these guidelines, financial institutions must submit a Suspicious

Activity Report (“SAR”) in connection with all

cannabis-related banking activities by any client of such financial

institution, in accordance with federal money laundering laws.

These cannabis-related SARs are divided into three categories -

cannabis limited, cannabis priority, and cannabis terminated -

based on the financial institution’s belief that the business

in question follows state law, is operating outside of compliance

with state law, or where the banking relationship has been

terminated, respectively.

The FinCEN Guidance states that in some circumstances, it is

permissible for banks to provide services to cannabis-related

businesses without risking prosecution for violation of federal

money laundering laws. It refers to supplementary guidance included

in the Cole Memorandum. The revocation of the Cole Memorandum has

not yet affected the status of the FinCEN Guidance, nor has the

United States Department of the Treasury given any indication that

it intends to rescind the FinCEN Guidance itself. Although the

FinCEN Guidance remains intact, it is unclear whether the current

administration or future administrations will continue to follow

the guidelines of the FinCEN Guidance. The DOJ continues to have

the right and power to prosecute crimes committed by banks and

financial institutions, such as money laundering and violations of

the Bank Secrecy Act, that occur in any state including states that

have in some form legalized the sale of cannabis. Further, the

conduct of the DOJ’s enforcement priorities could change for

any number of reasons. A change in the DOJ’s priorities could

result in the DOJ’s prosecuting banks and financial

institutions for crimes that were not previously

prosecuted.

In the event that any of the Company’s operations, or any

proceeds thereof, any dividends or distributions therefrom, or any

profits or revenues accruing from such operations in the United

States were found to be in violation of money laundering

legislation or otherwise, such transactions may be viewed as

proceeds of a crime under one or more of the statutes noted above

or any other applicable legislation. Apart from the consequences of

any prosecution in connection with such violation, among other

things, this could restrict or otherwise jeopardize the

Company’s ability to declare or pay dividends, effect other

distributions or subsequently repatriate such funds back to

Canada.

Restricted Access to Banking Services Could Make Operating our

Business and Maintaining our Finances Difficult.

The FinCEN Guidance, as further described above, remains effective

to this day, in spite of the fact that the Cole Memorandum was

rescinded and replaced by the Sessions Memorandum. The FinCEN

Guidance does not provide any safe harbors or legal defenses from

examination or regulatory or criminal enforcement actions by the

DOJ, FinCEN or other federal regulators, though. Thus, most banks

and other financial institutions in the U.S. do not appear to be

comfortable providing banking services to cannabis-related

businesses, or relying on this guidance, which can be amended or

revoked at any time by the current or future federal

administrations. In addition to the foregoing, banks may refuse to

process debit card payments and credit card companies generally

refuse to process credit card payments for cannabis-related

businesses. As a result, the Company may have limited or no access

to banking or other financial services in the U.S. The inability or

limitation in the Company’s ability to open or maintain bank

accounts, obtain other banking services and/or accept credit card

and debit card payments may make it difficult for the Company to

operate and conduct its business as planned or to operate

efficiently.

Heightened Scrutiny by Securities Regulatory Authorities in the

United States and Canada May Impact Investors’ Ability to

Transact in the Company’s Securities.

The Company’s existing operations in the United States, and

any future operations or investments, may become the subject of

heightened scrutiny by regulators, stock exchanges and other

authorities in the United States and/or Canada. As a result, the

Company may be subject to significant direct and indirect

interaction with public officials. It is impossible to determine

the extent of the impact of any new laws, regulations or

initiatives that may be proposed, or whether any proposals will

become law or otherwise be adopted, and there can be no assurance

that heightened scrutiny will not in turn lead to the imposition of

certain restrictions on the Company’s ability to operate or

invest in the United States or any other jurisdiction, in addition

to those described herein.

The Company’s operations in the United States cannabis market

may become the subject of heightened scrutiny by regulators, stock

exchanges, clearing agencies and other authorities in Canada. It

has been reported by certain publications in Canada that the

Canadian Depository for Securities Limited is considering a policy

shift that would see its subsidiary, CDS Clearing and Depository

Services Inc. (“CDS”), refuse to settle trades for

cannabis issuers that have investments in the United States. CDS is

Canada’s central securities depository, clearing and

settlement hub settling trades in the Canadian equity, fixed income

and money markets. CDS or its parent company has not issued any

public statement with regard to these reports. On February 8, 2018,

following discussions with the Canadian Securities Administrators

and recognized Canadian securities exchanges, CDS signed the CDS

Memorandum of Understanding (“MOU”) with The Aequitas

NEO Exchange Inc., the CSE, the Toronto Stock Exchange, and the TSX

Venture Exchange. The MOU outlines the parties’ understanding

of Canada’s regulatory framework applicable to the rules and

procedures and regulatory oversight of the exchanges and CDS as it

relates to issuers with cannabis-related activities in the United

States. The MOU confirms, with respect to the clearing of listed

securities, that CDS relies on the exchanges to review the conduct

of listed issuers. As a result, there currently is no CDS ban on

the clearing of securities of issuers with cannabis -related

activities in the United States. However, if CDS were to proceed in

the manner suggested by these publications, and apply such a ban on

the clearing of securities of the Company, it would have a material

adverse effect on the ability of the Company’s shareholders

to effect trades of shares through the facilities of a stock

exchange in Canada, as a result of which such shares could become

highly illiquid.

The Depositary Trust Company (“DTC”) is the primary

depository for securities in the United States. Several major U.S.

securities clearing companies that provide clearance, custody and

settlement services in the United States terminated providing

clearance services to issuers in the cannabis industry, including

those that operate entirely outside the United States, in response

to the Sessions Memo. As a result of these decisions, U.S.

securityholders may experience difficulties depositing securities

of cannabis companies in the DTC system or reselling their

securities in open market transactions, including transactions

facilitated through the CSE. Many larger U.S. broker-dealers own

U.S. securities companies that self-clear transactions. However,

some U.S. brokerages have adopted policies precluding their clients

from trading securities of cannabis issuers.

Changes in State or Federal Political/or Regulatory Climate Could

Impact the Company’s Business.

The success of the Company’s business strategy depends on the

legality of the cannabis industry in the states in which the

Company operates, and the lack of federal enforcement of its laws

that make cannabis businesses illegal. The political environment

surrounding the cannabis industry in general can be volatile and

the statutory and regulatory framework remains in flux. Despite

widespread state legalization, the risk remains that a shift in the

regulatory or political realm could occur and have a drastic impact

on the industry as a whole, adversely impacting the Company’s

business, results of operations, financial condition or

prospects.

Delays in enactment of or changes in new state regulations, or

changes in federal laws or enforcement priorities, could restrict

the Company’s ability to reach strategic growth targets and

lower return on investor capital. The strategic growth strategy of

the Company will be reliant upon state regulations being

implemented to facilitate the operation of medical and adult-use

cannabis in California. If such regulations are not timely

implemented, or are subsequently repealed or amended, or contain

prolonged or problematic phase-in or transition periods or

provisions, the Company’s ability to achieve its growth

targets, and thus, the return on investor capital, could be

adversely affected. The Company is unable to predict with certainty

when and how the outcome of these complex regulatory and

legislative proceedings will affect its business and

growth.

Further, there is no guarantee that state laws legalizing and

regulating the sale and use of cannabis will not be repealed or

overturned, or that local governmental authorities will not limit

the applicability of state laws within their respective

jurisdictions. If the federal government begins to enforce federal

laws relating to cannabis in states where the sale and use of

cannabis is currently legal, or if existing applicable state laws

are repealed or curtailed, the Company’s business, results of

operations, financial condition and prospects would be materially

adversely affected. It is also important to note that local and

city ordinances may strictly limit and/or restrict cannabis

businesses in a manner that will make it extremely difficult or

impossible to transact business that is necessary for the continued

operation of the cannabis industry, including the Company. Federal

actions against individuals or entities engaged in the cannabis

industry or a repeal of applicable cannabis related legislation

could adversely affect the Company and its business, results of

operations, financial condition and prospects.

The medical and adult-use cannabis industries are in their infancy

and the Company anticipates that the current California regulations

will be subject to change as California’s regulation of the

cannabis industry matures. The Company’s compliance program

emphasizes security and inventory control to ensure strict

monitoring of cannabis and other inventory from cultivation to sale

or disposal. Additionally, Lowell Farms has created standard

operating procedures that include descriptions and instructions for

monitoring inventory at all stages of cultivation, processing,

manufacturing, distribution, transportation and delivery. The

Company will continue to monitor compliance on an ongoing basis in

accordance with its compliance program, standard operating

procedures, and any changes to applicable regulation.

Overall, the medical and adult-use cannabis industry is subject to

significant regulatory change at each of the local, state and

federal level. The inability of the Company to respond to the

changing regulatory landscape may cause it to be unsuccessful in

capturing significant market share and could otherwise harm its

business, results of operations, financial condition or

prospects.

Investors Could Be Disqualified From Ownership in the

Company.

The Company’s business is in a highly regulated industry in

which many states have enacted extensive rules for ownership of a

participant company. Investors in the Company could become

disqualified from having an ownership stake in the Company under

relevant laws and regulations of applicable state and/or local

regulators, if the applicable owner is convicted of a certain type

of felony or fails to meet the requirements for owning equity in a

company like the Company.

Negative Public Opinion and Perception of the Cannabis Industry

Could Adversely Impact Our Ability to Operate and Our Growth

Strategy.

Government policy changes or public opinion may result in a

significant influence over the regulation of the cannabis industry

in Canada, the United States or elsewhere. The Company believes the

medical and adult-use cannabis industry is highly dependent on

consumer perception regarding the safety and efficacy of such

cannabis. Consumer perceptions regarding legality, morality,

consumption, safety, efficacy and quality of cannabis are mixed and

evolving. Public opinion and support for medical and adult-use

cannabis has traditionally been inconsistent and varied from

jurisdiction to jurisdiction. While public opinion and support

appears to be rising for legalizing medical and adult-use cannabis,

it remains a controversial issue subject to differing opinions

surrounding the level of legalization (for example, medical

cannabis as opposed to legalization in general). A negative shift

in the public’s perception of cannabis in the United States

or any other applicable jurisdiction could affect future

legislation or regulation. Among other things, such a shift could

cause state jurisdictions to abandon initiatives or proposals to

legalize medical and/or adult-use cannabis, or could result in

adverse regulatory changes in California, thereby limiting the

Company’s growth prospects and number of new state

jurisdictions into which the Company could expand. Any inability to

fully implement the Company’s expansion strategy may have a

material adverse effect on its business, results of operations or

prospects.

Significant Licensure Requirements and Limitations in States Where

Cannabis is Legal Could Impact the Company’s Ability to

Maintain its Operations.

The Company’s business is subject to a variety of laws,

regulations and guidelines relating to the cultivation,

manufacture, management, transportation, extraction, storage and

disposal of cannabis, including laws and regulations relating to

health and safety, the conduct of operations and the protection of

the environment. Achievement of the Company’s business

objectives are contingent, in part, upon compliance with applicable

regulatory requirements and obtaining all requisite regulatory

approvals. Changes to such laws, regulations and guidelines due to

matters beyond the control of the Company may cause adverse effects

to the Company.

The Company will be required to obtain or renew government permits

and licenses for its current and contemplated operations.

Obtaining, amending or renewing the necessary governmental permits

and licenses can be a time-consuming process involving numerous

regulatory agencies, involving public hearings and costly

undertakings on the Company’s part. The duration and success

of the Company’s efforts to obtain, amend and renew permits

and licenses will be contingent upon many variables not within its

control, including the interpretation of applicable requirements

implemented by the relevant permitting or licensing authority. The

Company may not be able to obtain, amend or renew permits or

licenses that are necessary to its operations. Any unexpected

delays or costs associated with the permitting and licensing

process could impede the ongoing or proposed operations of the

Company. To the extent permits or licenses are not obtained,

amended or renewed, or are subsequently suspended or revoked, the

Company may be curtailed or prohibited from proceeding with its

ongoing operations or planned renovation, development and

commercialization activities. Such curtailment or prohibition may

result in a material adverse effect on the Company’s

business, financial condition, results of operations or prospects.

California state licenses, and some local licenses, are renewed

annually. Each year, licensees are required to submit a renewal

application per guidelines published by the BCC (for state

licenses) or the applicable local regulatory body (for local

licenses), including the DCR. While renewals are annual, there is

no ultimate expiry after which no renewals are permitted.

Additionally, with respect to the renewal process, provided that

the requisite renewal fees are paid, the renewal application is

submitted in a timely manner and there are no material violations

noted against the applicable license, the Company would expect to

receive the applicable renewed license in the ordinary course of

business.

Under MAUCRSA, after January 1, 2018, only license holders are

permitted to engage in commercial cannabis activities. A

prerequisite to obtaining a California state license is obtaining a

valid license, permit or authorization from a local municipality.

The process associated with acquiring a permanent state license is

onerous and there are no assurances that the Company, or any

subsidiary or entity to which the Company will provide or intends

to provide services, will be granted any licenses or any renewals

thereof. Because there are different licenses for different types

of commercial cannabis activities, even if the Company, any

subsidiary and/or any such entity to which the Company will provide

services or intends to provide services is granted one or more

licenses, there are no assurances that they will be granted all of

the licenses they will need to effectuate the Company’s

business plan. Further, as part of the permitting and licensing

process in California, state and local officials may conduct both

random and scheduled inspections of cannabis operations. The

Company is required to comply with both state laws and regulations

and applicable local ordinances and codes. Compliance with both

state and local laws may be burdensome and failure to do so could

result in the loss of licenses, civil penalties and possibly

criminal prosecution. While the compliance controls of Lowell Farms

have been developed to mitigate the risk of any material violations

of any license it holds arising, there is no assurance that the

Company’s licenses will be renewed by each applicable

regulatory authority in the future in a timely manner. Any

unexpected delays or costs associated with the licensing renewal

process for any of the licenses held or to be held by the Company

could impede the ongoing or planned operations of the Company and

have a material adverse effect on the Company’s business,

financial condition, results of operations or

prospects.

The Company may become involved in a number of government or agency

proceedings, investigations and audits. The outcome of any

regulatory or agency proceedings, investigations, audits, and other

contingencies could harm the Company’s reputation, require

the Company to take, or refrain from taking, actions that could

harm its operations or require the Company to pay substantial

amounts of money, harming its financial condition. There can be no

assurance that any pending or future regulatory or agency

proceedings, investigations and audits will not result in

substantial costs or a diversion of management’s attention

and resources or have a material adverse impact on the

Company’s business, financial condition, results of

operations or prospects.

Reclassification of Cannabis in the United States Could Adversely

Impact the Company’s Business and Growth

Strategy.

If marijuana is re-categorized as a Schedule II or lower controlled

substance, the ability to conduct research on the medical benefits

of cannabis would most likely be improved; however, if cannabis is

re-categorized as a Schedule II or other controlled substance, and

the resulting re-classification would result in the requirement for

U.S. FDA approval if medical claims are made for the

Company’s products such as medical cannabis, then as a

result, such products may be subject to a significant degree of

regulation by the U.S. FDA and DEA. In that case, the Company may

be required to be registered (licensed) to perform these activities

and have the security, control, recordkeeping, reporting and

inventory mechanisms required by the DEA to prevent drug loss and

diversion. Obtaining the necessary registrations may result in

delay of the cultivation, manufacturing or distribution of the

Company’s anticipated products. The DEA conducts periodic

inspections of certain registered establishments that handle

controlled substances. Failure to maintain compliance could have a

material adverse effect on the Company’s business, financial

condition and results of operations. The DEA may seek civil

penalties, refuse to renew necessary registrations, or initiate

proceedings to restrict, suspend or revoke those registrations. In

certain circumstances, violations could lead to criminal

proceedings. Furthermore, if the U.S. FDA, DEA, or any other

regulatory authority determines that the Company’s products

may have potential for abuse, it may require the Company to

generate more clinical or other data than the Company currently

anticipates in order to establish whether or to what extent the

substance has an abuse potential, which could increase the cost

and/or delay the launch of that product.

Service Providers May Suspend or Withdraw Services if an Adverse

Change in Cannabis Regulation Occurs.

As a result of any adverse change to the approach in enforcement of

United States cannabis laws, adverse regulatory or political

change, additional scrutiny by regulatory authorities, adverse

change in public perception in respect of the consumption of

marijuana or otherwise, third party service providers to the

Company could suspend or withdraw their services, which may have a

material adverse effect on the Company’s business, revenues,

operating results, financial condition or prospects.

Increasing Legalization of Cannabis and Rapid Growth and

Consolidation in the Cannabis Industry may Further Intensify

Competition.

The cannabis industry is undergoing rapid growth and substantial

change, and the legal landscape for medical and recreational

cannabis is rapidly changing internationally. An increasing number

of jurisdictions globally are passing legislation allowing for the

production and distribution of medical and/or recreational cannabis

in some form or another. Entry into the cannabis market by

international competitors might lower the demand for our

products.

The foregoing legalization and growth trends in the cannabis

industry has resulted in an increase in competitors, consolidation

and formation of strategic relationships. Such acquisitions or

other consolidating transactions could harm us in a number of ways,

including by losing strategic partners if they are acquired by or

enter into relationships with a competitor, losing customers,

revenue and market share, or forcing us to expend greater resources

to meet new or additional competitive threats,all of which could

harm our operating results. As competitors enter the market and

become increasingly sophisticated, competition in the cannabis

industry may intensify and place downward pressure on retail prices

for products and services, which could negatively impact

profitability.

The Company May Encounter Difficulties Entering its Contracts in

Federal and Some State Courts.

Due to the nature of the Company’s business and the fact that

its contracts involve cannabis and other activities that are not

legal under federal law, the Company may face difficulties in

enforcing its contracts in federal and certain state courts. The

inability to enforce any of the Company’s contracts could

have a material adverse effect on the Company’s business,

operating results, financial condition or prospects. California

enacted a law that provides that notwithstanding any other law,

commercial activity relating to medicinal cannabis or adult-use

cannabis conducted in compliance with California law and any

applicable local standards, requirements, and regulations shall be

deemed to be all of the following: (1) a lawful object of a

contract, (2) not contrary to, an express provision of law, any

policy of express law, or good morals, and (3) not against public

policy.

The Company’s articles of incorporation provides that the

Supreme Court of the Province of British Columbia, Canada and the

appellate Courts therefrom are the sole and exclusive forum for any

derivative action brought on behalf of the company, which may limit

our investors’ flexibility in selecting a forum for any

future disputes.

Our articles of incorporation provides that the Supreme Court of

the Province of British Columbia, Canada and the appellate Courts

therefrom are the sole and exclusive forum for any derivative

action brought on behalf of the company. Our articles of incorporation do not limit the

ability of investors to bring direct actions outside of British

Columbia, Canada, including those arising under the Exchange Act

and the Securities Act. Section 27 of the Securities Exchange Act

of 1934, as amended (the “Exchange Act”), creates

exclusive federal jurisdiction over actions brought to enforce any

duty or liability created by the Exchange Act or the rules and

regulations thereunder, and Section 22 of the Securities Act of

1933, as amended (the “Securities Act”), creates

concurrent jurisdiction for federal and state courts over all suits

brought to enforce any duty or liability created by the Securities

Act or the rules and regulations thereunder. Neither investors nor

the Company and may waive compliance with the federal securities

laws and the rules and regulations thereunder, and it is therefore

uncertain whether the exclusive forum provision of our charter

would be enforced by a court as to derivative claims brought under

the Exchange Act or the Securities Act. Furthermore, the exclusive

forum provision of our charter may increase the costs to investors

in bringing claims, may discourage investors from bringing claims

and may limit investors’ ability to bring claims in a

judicial forum that they find favorable.

The COVID-19 Pandemic May Adversely Affect Our Business and

Financial Condition.

The COVID-19 pandemic has adversely impacted commercial

and economic activity and contributed to significant volatility in

the equity and debt markets in the U.S. and Canada. The impact of

the outbreak continues to develop and many jurisdictions, including

the State of California and local municipalities, have instituted

quarantines, prohibitions on travel and the closure of offices,

businesses, schools, retail stores and other public venues.

Individual businesses and industries are also implementing similar

precautionary measures. Those measures, as well as the general

uncertainty surrounding the dangers and effects

of COVID-19, have created significant disruption in

supply chains and economic activity. New strains of the virus have

been identified originating in the U.S. and elsewhere. These new

strains may have different transmission, morbidity and mortality

rates than the original virus, and the COVID-19 vaccines developed

to date may not be effective to provide immunization against new

strains of the virus. While the Company has continuously sought to

assess the potential impact of the pandemic on its financial

condition and operating results, any assessment is subject to

extreme uncertainty as to probability, severity and duration. The

continued spread of the virus globally could result in a protracted

world-wide economic downturn, the effects of which could last for

some period after the pandemic is controlled and/or abated and our

business, financial condition, results of operations and cash flows

could be materially adversely affected. The impact

of COVID-19 could have the effect of heightening many of

the other risk factors described herein.

The Company has attempted to assess the impact of the pandemic by

identifying risks in the following principle areas.

o

Price

Volatility. Since the COVID-19 outbreak commenced, the securities

markets in the U.S. and Canada have experienced a high level of

price and volume volatility and wide fluctuations in the market

prices of securities of many companies, which have not necessarily

been related to the operating performance, underlying asset values

or prospects of such companies. Future developments may adversely

impact the price of the Subordinate Voting Shares.

o

Mandatory

Closure . In California, the Company’s business has been

deemed an “essential service”, permitting the Company

to stay open despite the mandatory closure of non-essential

businesses. The Company continues to work closely with state and

local regulators to remain operational, but there is no guarantee

further measures may nevertheless require it to shut

operations.

o

Customer

Impact . While the Company has not experienced an overall downturn

in demand for its products in connection with the pandemic,

fluctuating rates of illness, as well as quarantining,

self-quarantining, “social distancing” and other

responsive measures, may have a material negative impact on demand

for its products while the pandemic continues. Certain of the

Company’s customers have altered operating procedures as a

result of the outbreak and the impact of such changes is being

monitored by the Company.

o

Supply

Chain Disruption . The Company relies on third party suppliers for

equipment and services to produce its products and keep its

operations going. If its suppliers are unable to continue operating

due to mandatory closures or other effects of the pandemic, it may

negatively impact its own ability to continue operating. At this

time, the Company has not experienced any failure to secure

critical supplies or services. However, disruptions in our supply

chain may affect our ability to continue certain aspects of the

Company’s operations or may significantly increase the cost

of operating its business and significantly reduce its

margins.

o

Staffing

Disruption . The Company is, for the time being, implementing among

its staff where feasible “social distancing” measures

recommended by such bodies as the Center of Disease Control, the

Presidential Administration, as well as state and local

governments. The Company has cancelled non-essential travel by

employees, implemented remote meetings where possible, and

permitted all staff who can work remotely to do so. For those whose

duties require them to work on-site, measures have been implemented

to reduce infection risk, mandating additional cleaning of

workspaces and hand disinfection, providing masks and gloves to

certain personnel. Nevertheless, despite such measures, the Company

may find it difficult to ensure that its operations remain staffed

due to employees falling ill with COVID-19, becoming subject to

quarantine, or deciding not to come to come to work on their own

volition to avoid infection. At certain locations, the Company has

experienced increased absenteeism due to the pandemic. If such

absenteeism increases, the Company may not be able, including

through replacement and temporary staff, to continue to operate in

some or all locations. In addition, the Company may incur increased

medical costs/insurance premiums as a result of these health risks

to its personnel.

o

Regulatory

Backlog . Regulatory authorities, including those that oversee the

cannabis industry on the state level, are heavily occupied with

their response to the pandemic. These regulators as well as other

executive and legislative bodies in California may not be able to

provide the level of support and attention to day-to-day regulatory

functions as well as to needed regulatory development and reform

that they would otherwise have provided. Such regulatory backlog

may materially hinder the development of the Company’s

business by delaying such activities as product launches, facility

openings and approval of any future business acquisitions, thus

materially impeding development of its business.

The Company is actively addressing the risk to business continuity

represented by each of the above factors through the implementation

of a broad range of measures throughout its structure and is

re-assessing its response to the COVID-19 pandemic on an ongoing

basis. The above risks individually or collectively may have a

material impact on the Company’s ability to generate revenue.

Implementing measures to remediate the risks identified above may

materially increase our costs of doing business, reduce our margins

and potentially result in or increase losses. While the Company is

not currently in financial distress, if the Company’s

financial situation materially deteriorates as a result of the

impact of the pandemic, the Company could eventually be unable to

meet its obligations to third parties, which in turn could lead to

insolvency and bankruptcy of the Company.

The regional stay home order, announced by the California

Department of Public Health on December 3, 2020, as supplemented by

an additional order executed on December 6, 2020, was issued to

apply across California on a regional basis in respect of certain

designated regions. It is required to go into effect in respect of

a particular region at 11:59 p.m. the day after such region has

been announced to have less than 15% ICU availability. Among other

implications in the event this order becomes effective in respect

of a region:

o

private

gatherings of any size are prohibited in such region,

o

all

individuals living in such region are required to stay home except

as necessary to conduct activities associated with the operation,

maintenance, or usage of critical infrastructure, as required by

law, or as specifically permitted by this order,

o

indoor

and outdoor restaurant dining, personal care services and indoor

recreational facilities are required to close in such

region,

o

critical

infrastructure sectors may operate in such region and must continue

to modify operations pursuant to the applicable sector guidance,

and

o

all

retailers in such region may operate indoors at no more than 20%

capacity and must follow the public health guidance for

retailers.

Apart from the conditions under which this stay home order is

required to be followed, California state counties may exercise

discretion to apply this order voluntarily.

The Company facilities are not currently subject to any stay home

orders. The Company’s cultivation, manufacturing and

distribution operations and the Company’s various suppliers

of raw materials or inputs are considered to be a part of the

essential infrastructure sectors and as such do not require a

reduction in their scope or amount of activity. The end purchasers

of products distributed by the Company, being cannabis retail

dispensaries located across California, may be or become subject to

this stay home order. They would nonetheless be able to continue to

operate curbside pick-up and delivery services and potentially

limited capacity indoor operations in order to effect the sale of

their products, as they too are considered essential businesses.

Nonetheless, the impact of this stay home order may be to lessen

the demand for the Company’s products. The extent to which

this stay home order may impact the Company’s business,

financial position, results of operations and cash flows is highly

uncertain and cannot be quantified at this time. The Company will

continue to monitor the impact of this stay home order and take

measures that alter its business operations as may be required by

federal, state or local authorities and/or that the Company deems

are in the best interests of its employees, customers, suppliers,

shareholders and other stakeholders.

Wildfire Risks in Certain Areas of California Could Adversely

Impact the Company’s Operations.

Certain areas of California, including certain areas nearby the

Company’s cultivation facility in Monterey County, can be

negatively impacted by wildfires. Wildfires can cause smoke and ash

to pass through greenhouse vents and cause cannabis plants to fail

testing. As a result, the Company will close the greenhouse vents

when needed to prohibit smoke and ash from entering the greenhouses

at its cultivation facility. However, closing the greenhouse vents

may cause elevated temperatures within the greenhouses and as a

result induced plant stress, thereby negatively affecting plant

yields. Wildfires can also cause essential sunlight to be blocked

out, thereby negatively affecting plant yields in another manner.

Overall, such wildfires can materially disrupt the Company’s

ability to harvest cannabis crops, significantly diminishing both

the size and quality of the crops harvested, the Company’s

supply chain, and other operations and as a result can negatively

impact the Company’s business, financial position, results of

operations and cash flows. Wildfires that occurred in late summer,

early fall 2020 negatively impacted the Company’s business,

financial position, results of operations and cash flows during the

third quarter of 2020 and are expected to continue to have a

negative impact for the fourth quarter of 2020 and potentially

beyond as the Company completes its production from cannabis crops

that were impacted by such wildfires that occurred earlier this

year. In the fourth quarter of 2020, the Company installed

automated environmental control systems within individual grow

rooms at its cultivation facility. While the Company believes that

the addition of such systems should mitigate future negative

effects of wildfires that may occur nearby the Company’s

cultivation facility, there is no guarantee that such negative

effects would in fact be mitigated. The extent to which any such

future wildfires or any other natural disaster impacts the

Company’s results will depend on future developments, which

are highly uncertain and cannot be predicted.

Risks Related to our Acquisitions

The anticipated benefits of the Lowell Acquisition may not be

realized or may take longer than expected to realize.

Historically, the Company and the Lowell brands businesses have

operated independently. The future success of the Lowell

Acquisition, including anticipated benefits, depends, in part, on

our ability to optimize our combined operations. The

optimization of our operations following the Lowell Acquisition

will be a complex and time-consuming process and if we experience

difficulties in this process, the anticipated benefits may not be

realized fully or at all, or may take longer to realize than

expected, which could have an adverse effect on us for an

undetermined period. There can be no assurances that we will

realize the potential operating efficiencies, synergies and other

benefits currently anticipated from the Lowell

Acquisition.

The integration of the Lowell brands businesses and the

Company’s historical operations may present material

challenges, including, without limitation:

o

combining

the leadership teams and corporate cultures of the Company and

Hacienda;

o

the

diversion of management’s attention from other ongoing

business concerns and performance shortfalls as a result of the

devotion of management’s attention to the integration of the

businesses;

o

managing

a larger combined business;

o

maintaining

employee morale and retaining key management and other employees at

the combined company;

o

retaining

existing business and operational relationships, and attracting new

business and operational relationships;

o

the

possibility of faulty assumptions underlying expectations regarding

the integration process;

o

consolidating

corporate and administrative infrastructures and eliminating

duplicative operations;

o

managing

expense loads and maintaining currently anticipated operating

margins; and

o

unanticipated

issues in integrating information technology, communications and

other systems.

Some of these factors are outside of our control, and any one of

them could result in delays, increased costs, decreases in the

amount of potential revenues or synergies, potential cost savings,

and diversion of management’s time and energy, which could

materially affect our financial position, results of operations,

and cash flows.

We may complete additional acquisitions, enter into new lines of

business and expand into new geographic markets and businesses,

each of which may result in upfront costs and additional risks and

uncertainties in our businesses.

We intend, if market conditions warrant, to grow our businesses by

acquiring additional businesses, expanding existing products lines,

entering into new product lines and entering new geographic

markets. Attempts to expand our businesses involve a number of

special risks, including some or all of the following:

o

the

required investment of capital and other resources;

o

the

diversion of management’s attention from our existing

businesses;

o

the

assumption of liabilities in any acquired business;

o

the

disruption of our ongoing businesses;

o

entry

into markets or lines of business in which we may have limited or

no experience;

o

compliance

with or applicability to our businesses of regulations and laws,

including, in particular, regulations and laws in new states and

localities, and a lack of experience in interacting with the

regulatory authorities responsible for enforcing these regulations

and laws; and

o

increasing

demands on our operational and management systems and

controls.

In addition, the acquisition of additional businesses would involve

some or all of the integration risks identified above with respect

to the Lowell Acquisition. Not all of our historical acquisitions

have been successful. Because we have not yet identified these

potential new acquisitions, product line expansions, and expansions

into new geographic markets or lines of business, we cannot

identify all of the specific risks we may face and the potential

adverse consequences on us and their investment that may result

from any attempted acquisition or expansion.

Loss of Foreign Private Issuer Status